SellTower Signals

Why this Major 900 MHz Merger is a Massive Security Breakthrough

Target Assets: Anterix Inc. (NASDAQ: ATEX) & NextNav Inc. (NASDAQ: NN)

Date: May 20, 2026

Strategic Focus: Next-Generation Spectrum, Satellite D2D, and National Security Resiliency Grid

1. Executive Summary: The Core Thesis

The macroeconomic demand for secure, un-hackable, and disaster-proof critical infrastructure networks has hit an inflection point. Following Big Tech’s recent multi-billion-dollar investments in low-band spectrum assets (such as Amazon’s landmark $11.57B deal with Globalstar), public equity markets are significantly mispricing the synergistic potential of a combination between Anterix (ATEX) and NextNav (NN).

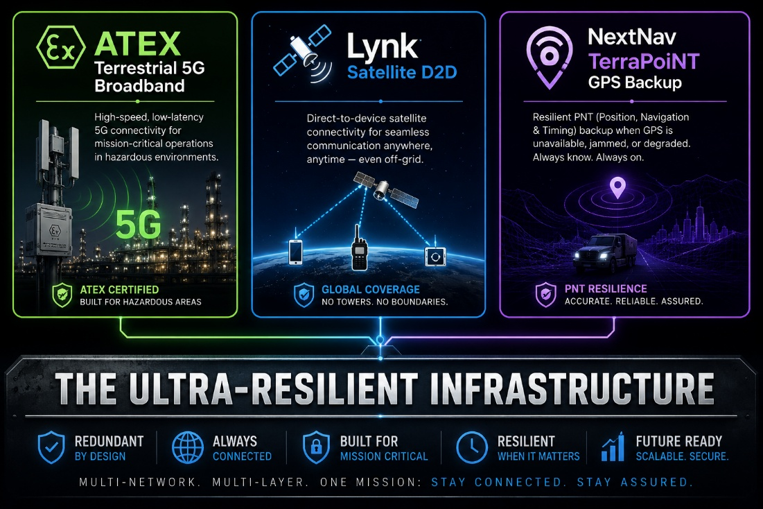

Historically viewed as siloed utility and geolocation plays, the macro landscape has fundamentally shifted. ATEX’s May 18, 2026 Federal Communications Commission (FCC) approval to test satellite Direct-to-Device (D2D) capabilities with Lynk Global signals that the company is transitioning from a “utility wireless provider” to a macro “ubiquitous critical infrastructure layer.” By merging with NextNav, the combined entity would create a contiguous 900 MHz low-band “super-grid” combining terrestrial 5G private broadband, satellite failover, and hardware-embedded GPS redundancy.

2. The Strategic Catalyst: The ATEX/Lynk Global Alliance

To understand the logic of an ATEX/NN pairing, investors must evaluate the strategic architecture established by ATEX’s experimental license approval:

- Spectrum Leap: The arrangement tests the implementation of Lynk’s satellite system inside ATEX’s licensed 900 MHz private wireless broadband spectrum.

- Beyond Mobile Phones: The trial explicitly expands the target market to include Land Mobile Radios (LMRs), enterprise routers, military hardware, and advanced edge-compute devices.

- Vertical Integration: This marks the framework for an autonomous, nationwide backup layer that operates fully independently of standard terrestrial carrier grids. It addresses a highly lucrative enterprise segment: electric/gas utilities, energy pipelines, long-haul logistics, and defense commands.

3. The Blueprint for the Pairing: Creating the “Super-Grid”

A corporate pairing between ATEX and NN merges three disconnected pillars into an irreplaceable national security asset:

Pillar A: Physical Spectrum Contiguity

- The Math: ATEX holds the 896-901/935-940 MHz bands. NextNav holds the directly adjacent 902-928 MHz band.

- The Synergy: A merger solves a massive engineering constraint for device manufacturers (e.g., Qualcomm). It allows a single piece of radio hardware or silicon chipset to span an unbroken, low-band footprint, bringing massive deployment cost efficiencies.

Pillar B: The Triad of Network Impermeability

Critical infrastructure clients require a “closed loop” network. If a hostile actor or natural disaster weaponizes cyber warfare or jams GPS satellites, the combined ATEX/NN ecosystem survives:

- Terrestrial Data: ATEX provides the secure private cellular lane.

- Space-Based Failover: Lynk routes data from low-Earth orbit when terrestrial cell towers fail.

- PNT Autonomy: NextNav’s TerraPoiNT provides terrestrial Positioning, Navigation, and Timing (PNT). If GPS goes dark, critical infrastructure—including grid substations, military bases, and logistics drones—retains location and microsecond-level synchronization.

Pillar C: Institutional Memory & Leadership Bridge

Corporate pairings usually fail on integration execution. Here, the bridge is already built. NextNav’s Chief Financial Officer, Tim Gray, is the former CFO of Anterix. He knows the asset base, the regulatory playbook, and the debt-equity plumbing of both entities intimately, dramatically lowering execution and integration risk.

4. Financial Profiles & Valuation Realities

An objective valuation reveals an asymmetric pair-trade or an attractive target for activist/private equity rollup.

| Metric | Anterix Inc. (NASDAQ: ATEX) | NextNav Inc. (NASDAQ: NN) |

| Market Capitalization | ~$1.10 Billion | High-growth, pre-revenue spectrum asset |

| Balance Sheet Status | Zero debt, strong cash position | High-burn rate, burdened by development debt |

| Near-Term Catalyst | Expanding utility contracts + Recent FCC 10 MHz broadband ruling (Feb 2026) | Pending high-stakes FCC Rulemaking Petition for 15 MHz broadband block |

| Revenue Model | Stable, multi-decade long-term leases | Pre-commercialization monetization of PNT network |

Financial Trade-Offs for Investors:

- The ATEX Advantage: ATEX is currently trading near its 52-week highs (~$57–$59) on the back of consecutive commercial wins and a favorable ruling expanding its 900 MHz band to a full 10 MHz of broadband. It represents the “stable currency” in this pairing.

- The NN Arbitrage: NextNav represents high-risk, asymmetric upside. It burns significant cash to build out its infrastructure. A merger protects NextNav from a costly standalone capital raise, while giving ATEX shareholders massive equity optionality on NextNav’s irreplaceable spectrum block.

5. Primary Risks & Regulatory Bottlenecks

While the industrial logic is pristine, investors must account for severe regulatory headwinds facing NextNav as of late Spring 2026:

- The Political Pushback: In April 2026, House Appropriators actively moved to introduce legislative barriers to block NextNav’s FCC proposal to reconfigure the 902-928 MHz band.

- Incumbent Interference Wars: Key industrial lobbies—ranging from electronic highway toll operators and railroads to commercial RFID chip manufacturers—are fighting NextNav’s 15 MHz broadband conversion, claiming it will cripple existing legacy automation networks.

- Dilution Risk for ATEX: Because ATEX boasts a clean, debt-free utility growth story, its institutional base may strongly resist absorbing NextNav’s high cash burn and regulatory legal battles unless the transaction is structured strictly as a stock-for-stock swap post-FCC clarity.

6. Strategic Conclusion & Investor Action Item

The Play: Speculative Accumulation via Monopolization Thesis.

An ATEX/NN standalone entity would likely not survive long on the public markets—and that is the exact goal. By consolidating the entire 900 MHz band, the combined entity creates a structural monopoly over sub-GHz spectrum tailored specifically for non-consumer, high-security macro applications.

This would position the combined firm as an ultimate take-private or acquisition target for global defense contractors (such as Lockheed Martin or Northrop Grumman), tier-one telecom equipment providers, or hyperscale cloud providers looking to sovereignize their edge-compute infrastructure.

Recommendation: Investors should maintain a core position in ATEX for stable capital appreciation tied to the utility sector, while using NextNav as a call-option vehicle. If NextNav clears its current regulatory hurdle with the FCC or undergoes a forced alignment with ATEX via institutional pressure, the combined spectrum value unlocks multiple multiples of the current standalone valuations.